1040 E-file: Appendix C - PIN Information

A PIN is required to e-file a 1040 return.

The Practitioner/Self-Select PIN program allows taxpayers to e-sign an e-filed return by selecting a five-digit Personal Identification Number (PIN).

Practitioner PIN

Advantages to using the Practitioner PIN program versus the Self-Select PIN program include:

- Prior-year AGI or prior-year PIN is not required.

- Birth dates are not required.

- First-time filers and tax payers under 16 are eligible.

EROs must complete Form 8878/8879 (including Part III) and retain this form for three years.

Taxpayer Eligibility Requirements for the Practitioner PIN Method

The following taxpayers are eligible to use this option:

- Taxpayers who are eligible to file Forms 1040, 1040A, 1040EZ, or 1040-SS (PR) for Tax Year 2020.

- Military personnel residing overseas with APO/FPO addresses.

- US Citizens and Resident Aliens residing in the US Possessions of the US Virgin Islands, Puerto Rico, America Samoa, Guam and the Commonwealth of the Northern Mariana Islands, or with foreign country addresses.

- Taxpayers filing Form 4868 (extension of time to file).

- Those who are filing on behalf of deceased taxpayers.

There is no age restriction on who can use the Practitioner PIN method; everyone who is eligible to e-file is eligible to use the Practitioner PIN method.

Self-Select PIN

Self-Select PIN for e-file is available for most taxpayers. EROs must complete Form 8878/8879 (including Part III) and retain this form for three years.

Taxpayers Eligible for Self-Select PIN

The following taxpayers are eligible to use the Self-Select PIN for e-file:

- Taxpayers who are eligible to file Form 1040, 1040A, 1040EZ, or 1040-SS (PR) for Tax Year 2020.

- Taxpayers who did not file for Tax Year 2019, but have filed previously.

- Taxpayers who are 16 or older on or before December 31, 2020, who have never filed a tax return.

- Primary Taxpayers under age 16 who have filed previously.

- Secondary taxpayers under age 16 who have filed in 2019.

- Military personnel residing overseas with APO/FPO addresses.

- US Citizens and Resident Aliens residing in the US Possessions of the US Virgin Islands, Puerto Rico, America Samoa, Guam, and the Commonwealth of the Northern Mariana Islands, or with foreign country addresses.

- Taxpayers filing Form 4868 (extension of time to file) or Form 2350 (extension for certain US citizens living abroad).

- Those who are filing on behalf of deceased taxpayers.

Taxpayers Not Eligible for Self-Select PIN

The following taxpayers are NOT eligible to participate:

- Primary taxpayers under age 16 who have never filed.

- Secondary taxpayers (spouse) under age 16 who did not file in 2019.

Using the Self-Select PIN

To use a Self-Selected PIN, taxpayers must furnish:

- their date of birth

- the Adjusted Gross Income from the 2019 return (before any adjustments) or the 2019 PIN or EFP. Only one must match IRS records.

Married Filing Joint Taxpayers

Married Filing Joint taxpayers are not required to use the same shared secret type. For example, the taxpayer can use the 2019 AGI and the spouse can use the 2019 PIN. Taxpayers who e-filed a 2019 tax return or extension can have multiple PINs on the IRS Master File. These taxpayers can use any of their prior year PINs to authenticate their entities and sign their tax returns or extensions using the Self-Select PIN method.

Taxpayers may provide both 2019 AGI and PIN but must match one to be authenticated.

Special Circumstances

If taxpayers filed a joint return for Tax Year 2019 and want to file separate returns for Tax Year 2020, they will each enter the same AGI or their PIN from the 2016 return on their separate returns for Tax Year 2020.

If taxpayers did not file jointly for Tax Year 2019, they are required to provide their respective AGI amount or PIN.

If a return was not filed for Tax Year 2019, the taxpayer is required to enter zero (0) in the AGI field. (The Prior Year PIN field should be left blank.)

If the taxpayer filed Form 1040PR for Tax Year 2019, the taxpayer is required to enter zero (0) in the AGI field. (The Prior Year PIN field should be left blank.)

Taxpayers who filed their 2019 tax return after December 7, 2020 are eligible to use the Self-Select PIN for e-file. However, these taxpayers will need to submit zeros for their Adjusted Gross Income. In the event that their return is rejected due to a mismatch of AGI, they can resubmit their return using their actual values. The extract creating the eligible Self-Select PIN file is created in December, and, due to processing constraints, late filers may or may not be included. Late filers can still use the Self-Select PIN.

Identity Protection Personal Identification Number (IP PIN)

Using the IP PIN (for Taxpayers)

If you reported to the IRS you were a victim of identity theft, use the IP PIN when you file your 2020 federal income tax return to avoid any delays.

Do not reveal your IP PIN to anyone other than a tax professional. Reveal it only for the purpose of preparing and e-filing your income tax return.

You may want to do the following:

- Review the information at Identity Theft and Your Tax Records (http://www.irs.gov/privacy/article/0,,id=186436,00.html).

- Review Publication 4535, Identity Theft Prevention and Victim Assistance (http://www.irs.gov/pub/irs-pdf/p4535.pdf).

Frequently Asked Questions

An updated list of frequently asked questions about IP PINs is located in the IP PIN section of the 1040 E-file FAQs, located at:

https://www.riahelp.com/html/2020/1040/content/1040_faqs/faq_1040_ef.htm

Tips for Next Year

You will receive a new IP PIN every year for three years after the identity theft incident. Use the new IP PIN when you prepare each year’s tax return.

Consider e-filing your taxes. E-filing can help you avoid mistakes and find credits and deductions that you may qualify for. In many cases you can file for free. Learn more about e-file at http://www.irs.gov/efile/index.html.

Using the IP Pin (for Tax Preparers)

If the following occurs:

- you are contacted by a taxpayer who received an IP PIN

- the taxpayer states that he or she is not the victim of identity theft

- your research does not indicate a reason for IP PIN issuance

inform the taxpayer of the following:

- Since an IP PIN was issued, it must be used to prevent any unnecessary delay in processing the tax return.

- A programming error caused some taxpayers to be identified as ID theft victims when they are not.

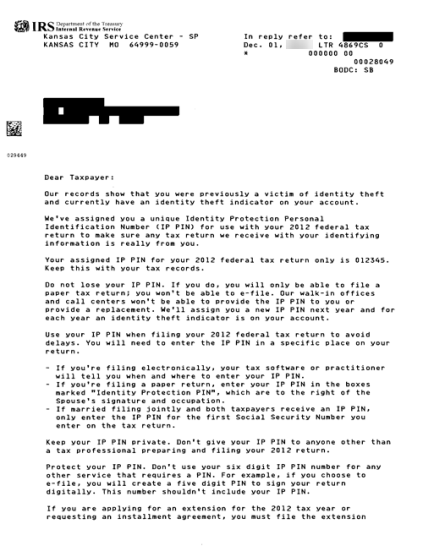

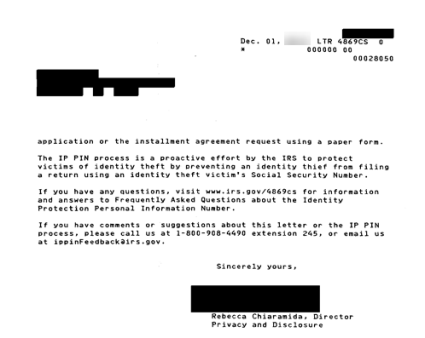

Understanding the IRS Letter

Each taxpayer’s letter may look different from the sample because the information contained in each letter is tailored to the individual taxpayer.

E-file/1040_ef_app_c_pin_information.htm/TY2020

Last Modified: 06/12/2020

Last System Build: 09/13/2021

©2020-2021 Thomson Reuters/Tax & Accounting.